|

|

Recent Articles

-

Dick’s Sporting Goods Still Looks Really Cheap

Dick’s Sporting Goods Still Looks Really Cheap

Nov 20, 2023

-

Image Source: Dick’s Sporting Goods.

On November 21, Dick’s Sporting Goods reported solid third-quarter results with sales up 2.8% on a year-over-year basis thanks to comparable store sales growth of 1.7% that lapped an impressive 6.5% increase in the same period a year ago. Non-GAAP earnings per share came in at $2.85 in the quarter, up from $2.60 in last year’s period. The company also raised its 2023 comparable store sales growth guidance range to 0.5%-2% from flat to 2% previously, and it raised its 2023 non-GAAP earnings per share outlook to $12.00-$12.60 from its previous range of $11.50-$12.30. We liked the news and continue to believe that shares are mispriced. Our fair value estimate stands at $160 per share, well above where shares are trading at the moment.

-

REITs Will Likely Continue To Underperform

REITs Will Likely Continue To Underperform

Nov 17, 2023

-

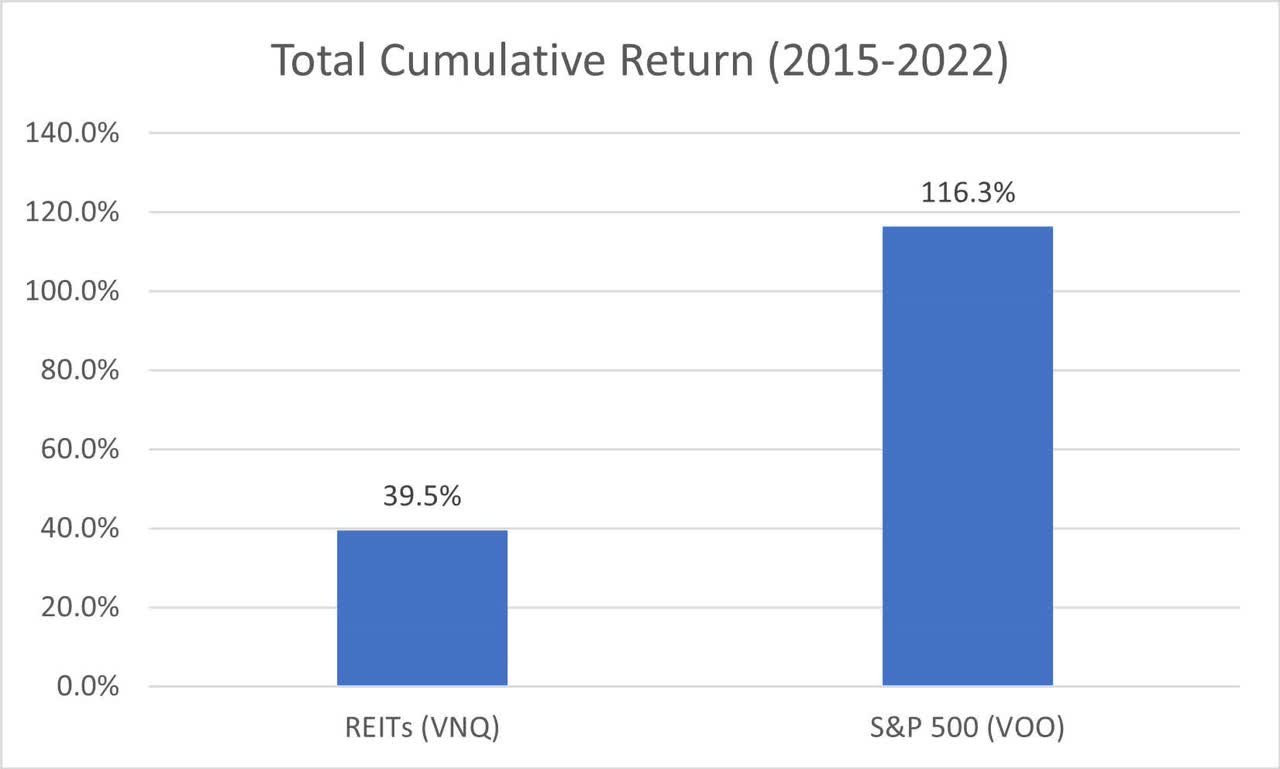

Image: REITs have not performed as well as some may have thought.

This article clearly explains that REIT dividends are risky and showcases that REIT investors have missed out on a lot of total return during the past decade or so. One has to go back a long time to see any real return from REITs, and changing working and shopping habits will likely continue to punish the broader REIT sector. We view REITs as a game of financial leverage tied to the vicissitudes of the commercial real estate cycle, all for a dividend yield that approximates that of risk-free assets these days. REITs seem to have a large following these days and many will come to the defense of REITs in their own way, but from a bird's eye view of this market, we remain puzzled by the love affair some have for them. We can only posit that some have a myopic focus on REIT-specific metrics, are not getting the best information when it comes to capital-market dependence risk, and perhaps don't truly understand the structural dynamics of the dividend payment with respect to the free dividends fallacy (i.e. that a REIT's share price is adjusted downward by the amount of the dividend on the ex-dividend date). In our view, the structural dynamics that have hurt REITs for the past decade won't be going away anytime soon, and for investors looking to maximize their returns and the longevity of their retirement savings, there are much better options than REITs.

-

Dividend Increases/Decreases for the Week of November 17

Nov 17, 2023

-

Let's take a look at firms raising/lowering their dividends this week.

-

Concerns Over Walmart’s Outlook Overblown

Nov 16, 2023

-

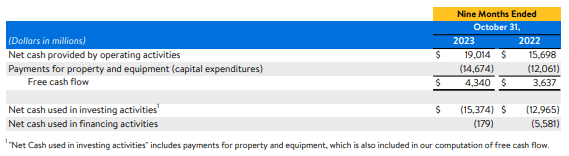

Image: Walmart’s free cash flow generation during the first nine months of its fiscal year has shown a nice jump.

On November 16, Walmart reported third quarter results for fiscal 2024 that showed revenue growth of 5.2% and adjusted operating income expansion of 3%. Adjusted earnings per share nudged up 2% in the quarter on a year-over-year basis. Operating cash flow during the first nine months of the year came in at $19 billion (up $3.3 billion from the year ago period), while free cash flow came in at $4.3 billion (up $0.7 billion on a year-over-year basis). The big box retailer ended the period with a ~$43.2 billion net debt position and has bought back 8.7 million shares of stock on a year-to-date basis. Walmart raised its outlook for the remainder of fiscal 2024, but its targets came in a bit shy of expectations. With shares trading down following the report, we think the market is overreacting. We won’t be making any changes to our $160 per share fair value estimate.

|