|

|

Recent Articles

-

Lithium Prices Remain Volatile; Albemarle Adjusts Long-term Demand Forecast

Lithium Prices Remain Volatile; Albemarle Adjusts Long-term Demand Forecast

Feb 21, 2024

-

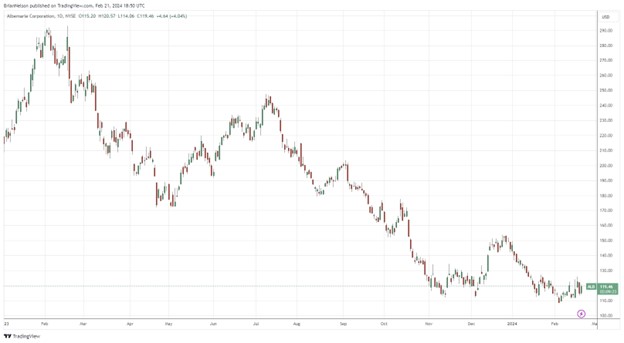

Image: Albemarle’s shares have faced significant pressure as a result of depressed lithium prices.

Albemarle’s shares have been under significant pressure of late due to volatile lithium prices, and the firm’s cash flows have faced weakness as a result. Operating cash flow dropped to ~$1.325 billion in 2023 from ~$1.91 billion in 2022, as capital spending soared. Unless lithium prices start to better reflect the underlying demand profile ahead of it, Albemarle will likely be free cash flow negative in 2024 as well. Right now, Albemarle is facing a tough road ahead with its fundamentals largely tied to lithium prices, but the firm is positioned well for a potential lithium-price rebound. Regardless, we view Albemarle as a speculative stock and one only for the most aggressive, risk-seeking investors.

-

Public Storage Puts Up Record Revenue and Net Operating Income in Fourth Quarter

Feb 21, 2024

-

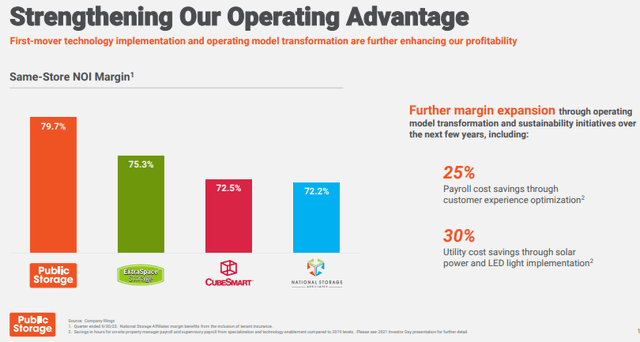

Image Source: Public Storage.

Self-storage giant Public Storage reported solid fourth quarter results February 20, with revenue and funds from operations [FFO] coming in better than expectations. The company is one of our favorite income-oriented ideas. It has now been in business for more than 50 years, and it boasts an enviable A2/A credit rating, allowing it easy access to the capital markets to fund future deals and projects. Public Storage’s same-store operating margin also runs higher than many of its peers, showcasing its more efficient operating model. We like Public Storage quite a bit, and the company yields ~4.2% at the time of this writing.

-

Walmart’s Free Cash Flow Remains Robust, Buys Vizio to Boost Advertising Business

Feb 21, 2024

-

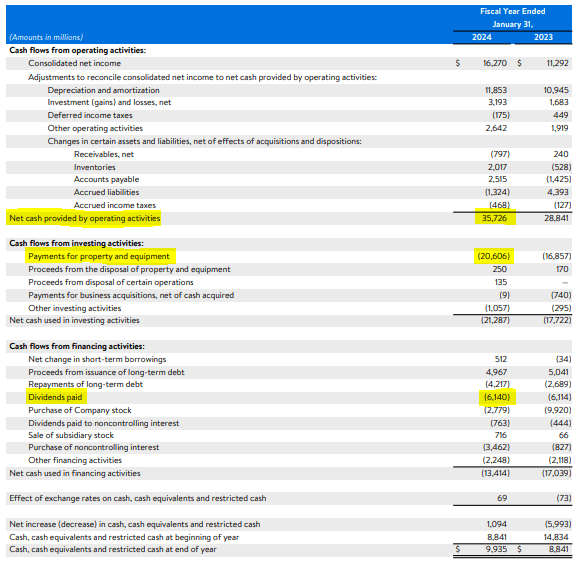

Image: Walmart’s free cash flow generation during fiscal 2024 was superb and comfortably covers its cash dividends paid.

Walmart is doing a fantastic job executing on its value proposition, and the company is in a sweet spot with respect to consumer trends given the step change in prices the past few years that is causing consumers to trade down to value offerings. The firm’s comp sales are coming in better than expected, and its free cash flow generation remains well in excess of its cash dividends paid, providing ample support for further dividend hikes. Walmart will execute a 3-for-1 stock split on February 23 and will begin trading on a post-split basis February 26. Though Walmart retains a massive net debt position, perhaps its only drawback from a financial standpoint, the company is a fantastic dividend grower and perhaps one of the best considerations within the retail space these days. Shares yield ~1.4% at the time of this writing.

-

Dividend Growth Idea Home Depot Hikes Payout Nearly 8%!

Feb 20, 2024

-

Image: Home Depot is working through some soft sales trends following robust home improvement spending during the pandemic, but the company’s free cash flow generation remains top notch.

On February 20, Dividend Growth Newsletter portfolio holding Home Depot reported mixed fourth quarter results that showed revenue pressure in the period, but the company still beat expectations on both the top and bottom lines. We’re huge fans of Home Depot’s resilience through the ups and downs of the real estate market, and the company’s pace of dividend growth remains solid. Our fair value estimate of Home Depot stands at $369 per share, modestly higher than where it is trading, and the company has a strong 1.4x Dividend Cushion ratio, which speaks to future dividend expansion.

|