|

|

Recent Articles

-

Best Buy Puts Up Best Comp Growth in Three Years

Best Buy Puts Up Best Comp Growth in Three Years

Aug 28, 2025

-

Image Source: TradingView.

We liked that Best Buy put up its strongest comparable store sales growth in the past three years, with domestic comparable online sales growth of 5.1%, lapping a decline of 1.6% in last year’s quarter. As a percentage of total domestic revenue, online revenue now accounts for 32.8% versus 31.5% last year. For the six month period ended August 2, cash flow from operations was $783 million, while capital spending was $341 million, resulting in free cash flow of $442 million, higher than its cash dividends paid of $403 million over the same time period. Best Buy covers dividends paid while it boasts a net cash position on the balance sheet. Shares yield 5% at the time of this writing.

-

AT&T Is Targeting Free Cash Flow in the Low-to-Mid $16 Billion Range for 2025

Aug 28, 2025

-

Image Source: TradingView.

Looking to the full year 2025, AT&T expects consolidated service revenue growth in the low-single-digit range, with mobility service revenue growth of 3% or better and consumer fiber broadband revenue growth in the mid-to-high teens. For the year, AT&T is targeting adjusted EBITDA growth of 3% or better, with mobility EBITDA growth of roughly 3%, business wireline EBITDA lower by a low-double-digit range, and consumer wireline EBITDA growth in the low-to-mid-teens range. Free cash flow for 2025 is expected in the low-to-mid $16 billion range, while adjusted earnings per share is targeted in the range of $1.97-$2.07. We like AT&T but can’t get comfortable with its total debt load of $132.3 billion. We remain on the sidelines. Shares yield 3.8% at the time of this writing.

-

Nvidia Shines in Second Quarter of Fiscal 2026

Aug 27, 2025

-

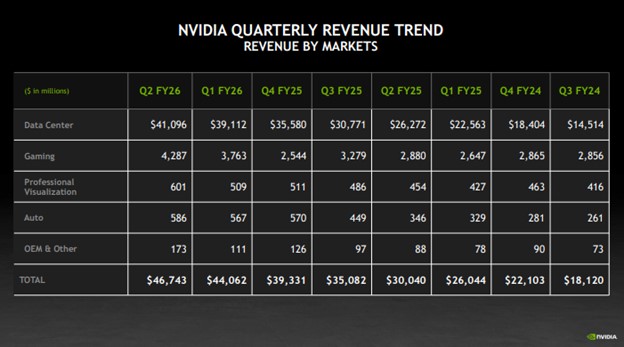

Image Source: Nvidia.

Looking to the third quarter of fiscal 2026, Nvidia expects revenue to be $54.0 billion, plus or minus 2%, an outlook that does not assume any H20 shipments to China. Consensus was at $52.76 billion. In the fiscal third quarter, GAAP and non-GAAP gross margins are expected to be 73.3% and 73.5%, respectively, plus or minus 50 basis points. The firm expects to end the year with non-GAAP gross margins in the mid-70% range. Nvidia continues to power the market higher, and while results weren’t as bullish as some were expecting, they were strong, nonetheless.

-

Dividend Increases/Decreases for the Week of August 22

Dividend Increases/Decreases for the Week of August 22

Aug 22, 2025

-

Let's take a look at firms raising/lowering their dividends this week.

|