|

|

Recent Articles

-

Taiwan Semiconductor’s Revenue Performance Is Fantastic

Taiwan Semiconductor’s Revenue Performance Is Fantastic

Jul 19, 2025

-

Image Source: Taiwan Semi.

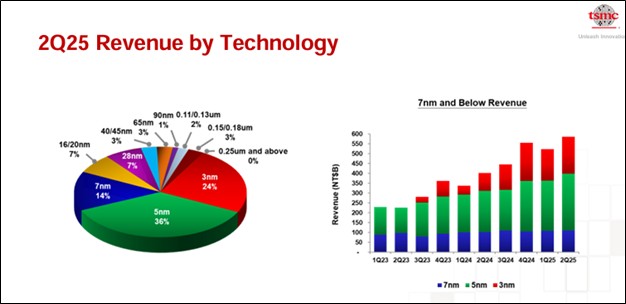

In the second quarter, TSM’s shipments of 3-nanometer accounted for 24% of total wafer revenue, while 5-nanometer accounted for 36%, and 7-nanometer accounted for 14%. Advanced technologies, defined as 7-nanometer and more advanced technologies, accounted for 74% of total wafer revenue. The company ended the quarter with NT$2,634.43 billion in cash and marketable securities and NT$883.67 billion in long-term interest-bearing debts. Free cash flow was NT$199.85 billion in the quarter, up from NT$171.99 billion in the second quarter of 2024. We liked TSM’s second quarter results and third quarter guidance and continue to like shares in the ESG Newsletter portfolio.

-

Dividend Increases/Decreases for the Week of July 18

Dividend Increases/Decreases for the Week of July 18

Jul 18, 2025

-

Let's take a look at firms raising/lowering their dividends this week.

-

ASML Cannot Confirm Growth in 2026 at This Stage

Jul 16, 2025

-

Image: ASML's shares fell under pressure following uncertainty regarding expected 2026 performance.

ASML’s second quarter results were solid, and we liked its sequential bookings growth in the quarter. The company’s revenue and gross margin guidance for the third quarter was also good, but margins look to face some pressure on a sequential basis. During the quarter, ASML repurchased around €1.4 billion worth of shares. Though we thought performance by the firm was great in the quarter, management’s commentary that it could not confirm growth in 2026 at this stage left something to be desired. We continue to be positive on ASML’s shares, nonetheless.

-

Key Comments from the Banks This Earnings Season

Jul 16, 2025

-

Image: The big banks have done well recently.

Let's read through key comments from banking executives this earnings season.

|